.png?width=400&height=85&name=Untitled%20(2).png)

Contents

What do the special VAT rules mean for the importation of low value goods into Ireland / EU?

What do the special VAT rules mean for the role of online marketplaces and platforms?

Introduction

Low value consignments (LVC) are consignments valued at £135 (€150) or less. The EU’s Import VAT Exemption and the UK’s Low Value Consignment Relief have been abolished. This means that import VAT is payable on all imports into the EU and the UK, regardless as to the value of the import.

There are a number of VAT rules associated with the cross-border movement of low value goods which traders in Ireland and Northern Ireland should be aware of.

What do the special VAT rules mean for the importation of low value goods into Ireland / EU?

Prior to the introduction of the July 2021 EU VAT e-commerce reform, when goods were imported into the EU / Northern Ireland, import VAT was paid at the point of importation (unless Postponed VAT Accounting was utilised). However, the 2021 VAT reform means that there are now two additional options for the payment of import VAT on consignments which do not exceed €150 / £135 in value:

1. Import One Stop Shop (IOSS): Under the IOSS, suppliers based in 3rd countries and selling goods to customers in EU/NI charge VAT on goods at the point of sale. The EU/NI based customer pays VAT as part of the purchase price of the goods. The subsequent movement of goods into the EU does not attract further import VAT liability.

Prior to the sale, the seller will register for the IOSS which allows them to charge EU VAT (at the appropriate rate that applies in the country to which the goods are being imported) to the customer upon sale. The seller is then responsible for declaring and paying the VAT collected to the EU tax authorities where the company is registered for the IOSS monthly.

2. Special arrangement for declaration and payment of import VAT: Where the IOSS is not utilised, it is possible to use the new simplification measure which has been introduced with a particular focus on postal operators, express carriers and other customs agents in the EU (i.e., the declarant). It is acknowledged that these individuals regularly declare low value goods for importation.

Under this option, VAT is not paid at check-out. Instead, the customer pays the VAT to the declarant presenting the goods to customers. The steps involved when using this option are shown below:

Step One |

Step Two |

Step Three |

Step Four |

| Goods from outside the EU are ordered by the customer. | The goods declared at import by declarant on behalf of the customer. | VAT is paid by the customer to declarant and the goods are delivered. | The declarant pays VAT collected by 16th of the next month. |

What do the special VAT rules mean for the role of online marketplaces and platforms?

Where online marketplaces or platforms are facilitating certain supplies of goods, they will be deemed to be making the supplies themselves. The relevant supplies are as follows:

- The importation of goods from outside the EU in consignments of an intrinsic value not exceeding €150 regardless of where the underlying supplier is established and/or

- Intra-EU distance sales of goods and domestic supplies of goods, regardless of the value of the goods, but where the underlying supplier is established outside of the EU.

As such, the online marketplace or platform will be responsible for accounting for the VAT on those supplies. This means that the supply of goods from an underlying supplier to an end customer, through an online marketplace or platform, will be artificially split into two supplies:

• A supply from the underlying supplier to the online marketplace or platform, and

• A supply from that online marketplace or platform to the customer.

Where an online marketplace or platform is deemed to be making supplies of goods, they will be treated as any other supplier of goods.

The online marketplace or platform can therefore opt to register to apply the Union scheme or the IOSS or both, depending on the supplies they are making. The rules of those schemes apply in the same way to that online marketplace or platform as they do to other suppliers using those schemes.

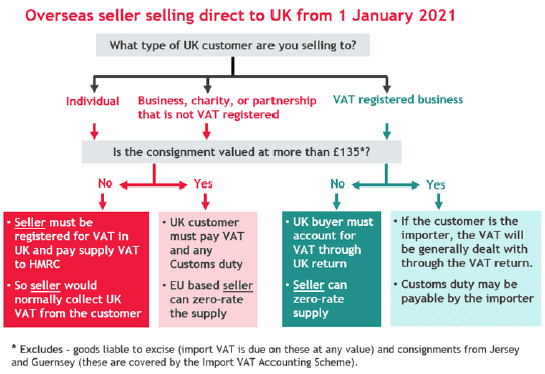

What do the special VAT rules mean for the sale of low value goods from the EU to GB based customers?

Consignments of goods with a value of £135 or less that are outside the UK and sold directly to customers (not through an online marketplace) in Great Britain (England, Scotland and Wales) will have UK VAT charged at the point of sale. This means Irish traders selling B2C to GB will have to register for UK VAT if selling goods valued at less than £135.

The rate of VAT to be charged is the rate that would apply if the goods had been supplied domestically in the UK.

The £135 limit applies to the value of a total consignment that is imported, not the separate value of individual items that are in a consignment. Also note that these new rules do not apply to excise goods or to non-commercial goods, such as gifts.

The only exception to the above rule is where the sale is a business-to-business sale, and the UK customer has provided the EU supplier with their UK VAT registration number. In this case, the reverse charge will apply, and the UK based business customer will be responsible for accounting for any VAT due on their UK VAT return.

Below is a flow chart to help a supplier understand what VAT rules to apply:

Article reviewed: August 2024