.png?width=400&height=85&name=Untitled%20(2).png)

Contents

Introduction

How is the origin of goods determined?

What does the free trade agreement mean?

How do I claim preference using rules of origin?

What happens with goods that do not meet the EU-UK TCA’s rules of origin?

What do I need to know to claim preferential rates of duty?

What actions do I need to take to claim preferential rates of duty?

Why is the Country of Origin required for goods that I import, and is this the same as the Country of Export?

How can I check the origin of my goods?

Further information

Introduction

Rules of origin play a key role in the movement of goods and help businesses determine where their goods originate from, and which goods are covered within current Free Trade Agreements (FTA). Rules of origin are necessary to ensure that the products that will benefit from the terms of an FTA (zero or reduced tariffs/quotas) are either manufactured in or wholly obtained from the country they are being exported from or sufficiently processed in that country.

How is the origin of goods determined?

Firstly, businesses must determine what good is being traded by identifying the correct commodity code. Once the code has been determined, businesses must establish the "economic nationality" of the goods, as opposed to identifying the country in which the goods were bought, re-packaged, or shipped from. This involves determining the value of the goods and where value has been added to produce the final product. If all materials were obtained and processed in one country, the goods would be classed as "wholly obtained" in that country, i.e., agricultural produce. To confirm, if a product is wholly obtained in the EU or UK, or produced exclusively from originating materials, it will be considered as originating in the EU or UK.

What does the free trade agreement mean?

The EU-UK / UK-EU Trade and Cooperation Agreement provides for zero tariffs and zero quotas on all goods that comply with the appropriate rules of origin. GOV.UK has detailed guidance on the rules of origin requirements that explains the most important provisions which businesses need to understand and comply with, in order to ensure that they pay zero tariffs when trading with the EU. This applies to both businesses that wish to export goods to the EU at zero tariffs, as well as businesses who wish to import goods from EU at zero tariffs. Businesses can claim preferential origin for EU-UK manufactured goods that meet the relevant rules of origin criteria, allowing businesses to benefit from zero or reduced tariffs/quotas as a key benefit of the free trade agreement between the EU and the UK.

How do I claim preference using rules of origin?

Preference can be claimed when the importer makes a claim to the customs authority receiving the goods for goods that originate in the partner country and meet the conditions of the TCA.

Within the TCA, a claim can be made if the importer has one of the following proofs of origin:

- A statement on origin that the product is originating, made out by the exporter

- Importer’s knowledge that the product is originating from the claimed country of export

Businesses can claim preference for different goods on the same document. The goods must be clearly marked that are originating and non-originating. There is no fixed method for doing this - the only requirement is that those goods are clearly indicated on the relevant documentation.

What happens with goods that do not meet the EU-UK TCA’s rules of origin?

Goods that do not meet the rules of origin requirements will not qualify for tariff preferences and will have to pay the standard "Most Favoured Nation" tariffs. The EU and UK’s rules of origin apply to imports from countries that have no free trade agreement in place.

What do I need to know to claim preferential rates of duty?

EU businesses that trade with businesses within GB must ensure they have an understanding of the following information to benefit from preferential rates of duty:

-

The type of good(s)

The first need is to determine what good is being traded. To do this you’ll need a unique code called a commodity code. For the purposes of rules of origin, you may only need the first four digits of the commodity code. But it’s important to note the length of the full code, as these are different for imports (ten digits) and exports (eight digits).

Getting the right commodity code is fundamental and it is the legal obligation of the trader. If you rely on the commodity code from a supplier, you’ll need to check it is accurate.

For more information about commodity codes and how to get them, read our guide to commodity codes.

-

The country the goods are being imported to

This should be straightforward. Once you know this, you’ll be able to determine what specific requirements are associated with that country.

-

Where the product judged to have originated from

There are two main categories of origin in the rules:

1. Goods wholly obtained or produced in a single country will be deemed to have originated in that country.

2. Where a product has been produced using materials from more than one country, the product origins shall be determined to be where the last substantial transformation took place.

Once a product has gained originating status, it is considered 100% originating. If the product is subsequently incorporated in the creation of a further product, its full value is considered originating, and no account is taken for non-originating materials within it. You could apply for binding origin information, which is a non-mandatory process that allows businesses to identify the appropriate origin of their goods. It can be particularly helpful where there are complex supply chains, with inputs from around the world. If this is the case, Binding Origin Information decisions are legally binding in that Customs territory.

Helpful links:

- GOV.UK: How to get a decision on the origin of your goods in the UK.

- Revenue.ie: Binding origin information in Ireland.

- GOV.UK: How to get a decision on the origin of your goods if you import into or export from Northern Ireland.

What actions do I need to take to claim preferential rates of duty?

There are some important actions you’ll need to take in order to benefit from preferential rates of duty.

-

Documentation

To benefit from preferential rates of duty, the importer is required to claim this treatment at the point of import and hold evidence that the goods comply with the rules of origin. An importer can do so if it has either a statement on origin (from the exporter) or knowledge (obtained and held by the importer) that the product is originating.

The exporter has an obligation to obtain a Supplier’s Declaration when they are not the producer of the goods. The declaration describes the non-originating materials in sufficient detail to enable them to be identified. Depending on your situation you may need one or both of the documents listed below:

-

Statement on origin

The exporter can self-declare the origin of a product by completing a statement on origin.

For EU exporters if the value of the consignment is less than €6,000, any EU exporter can self-declare that the product originates in the EU. If the value of the consignments is €6,000 and above, exporters in the EU need to be registered in the Registered Exporter System (REX) – Ireland here and Northern Ireland here - in order to self-declare that the product originates in the EU.

GB exporters are not required to hold an approved authorisation status to provide statements on origin, regardless of the value. They must include their EORI number in any statement on origin issued to their EU customer.

The statement on origin must be provided on an invoice or any other commercial document (excluding a bill of lading), describing the originating product in sufficient detail to enable them to be identified).

-

Supplier's declaration

The exporter may need to obtain a supplier's declaration (or equivalent document containing the same information) that describes the non-originating materials in sufficient detail to enable them to be identified. A supplier’s declaration can never be used as a document on origin for claiming preferential treatment at importation.

A supplier’s declaration should be made out for each consignment of products and attached to the invoice (or other document describing the products concerned in sufficient detail to enable them to be identified).

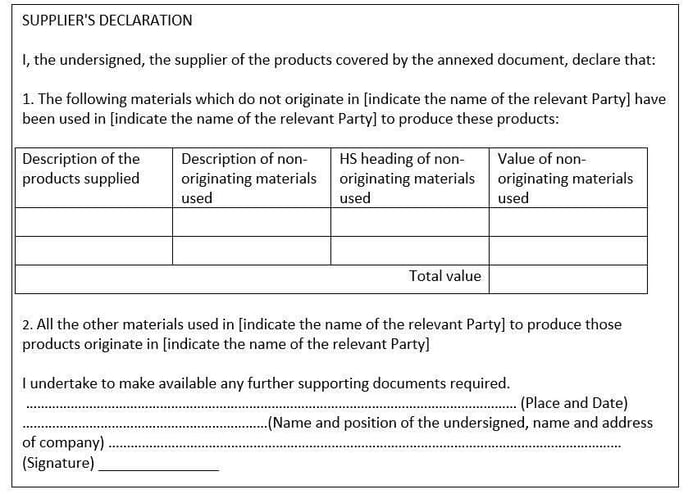

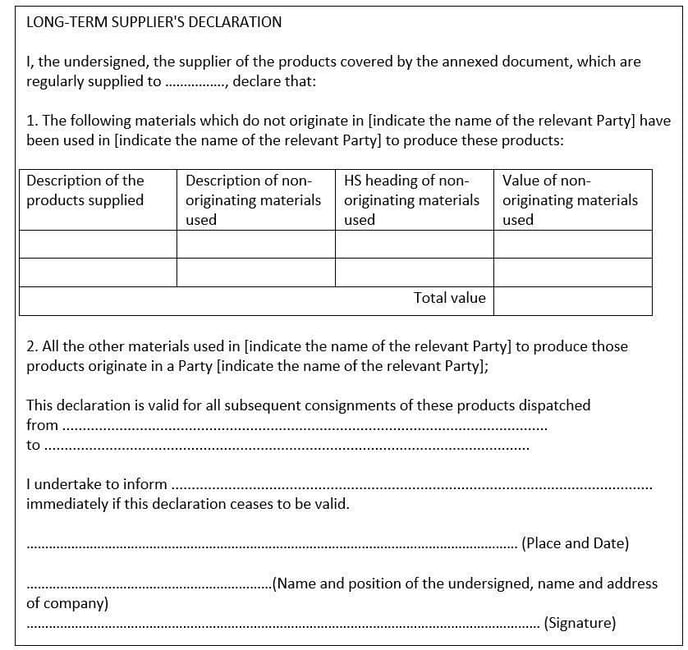

Where a supplier regularly supplies a customer with products (for which the production carried out is expected to remain constant for a period of time), that supplier may provide a single Supplier’s Declaration to cover subsequent consignments (the ‘long-term Supplier’s Declaration’). It is normally valid for a period of up to two years.

The images below show a Supplier's Declaration on the left and a Long-term Supplier's Declaration on the right.

|

|

Why is the Country of Origin required for goods that I import, and is this the same as the Country of Export?

Imports and exports are identified and regulated by both the commodity code for the item and its Country of Origin.

Rules of Origin are important in international trade as, in combination to the products commodity code, they can determine – based on trade regulations and agreements – how much duty is payable on the item and even, whether or not, certain products can be imported into a country.

The U.K. EU Trade & Cooperation Agreement (TCA) grants preferential origin and applies zero rate tariffs to U.K. origin goods moving to the EU and, vice-versa, EU origin goods moving to the U.K., however, in order to qualify for these preferential rates, a product must meet the rules of origin set out in the agreement:

- Wholly obtained: The product is entirely sourced in the UK or EU

- Produced exclusively: The product is made solely from materials that originate in the UK or EU

- Substantially transformed: The product has been sufficiently transformed in the UK or EU, in accordance with the product-specific rules in Annex 3

As per the requirements outlined above to determine origin, the country of export will not necessarily be the same as the country of origin.

How can I check the origin of my goods?

The European Commission offer a Self-Assessment Tool to help businesses in Northern Ireland / Ireland to ascertain the origin of their products. This can be accessed here: Access2Markets.

Further information

- GOV.UK: All the guides on rules of origin, to find out if you can reduce the duties on goods you import or export.

- European Commission:

Guidance on rules of origin.

- European Commission: PDF of EU-UK TCA Guidance on “Section 2: Origin Procedures"

- Revenue.ie: Helpful information on preferential and non-preferential origin.

- Chambers Ireland:

Information on whether Certificates of Origin are required when exporting to the UK and some Frequently Asked Questions.

Prepared by the InterTradeIreland Trade Hub Team.

Article reviewed: April 2025